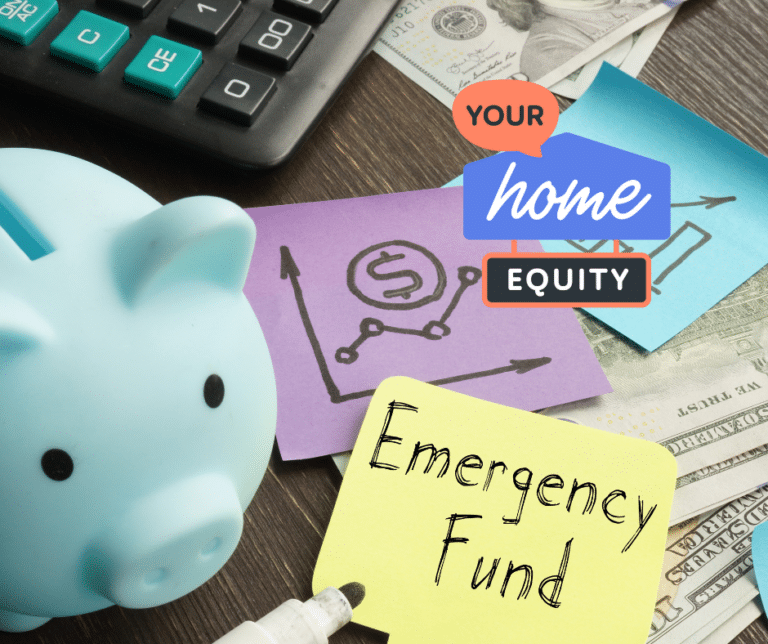

As we move into 2026, the preference for ‘ageing in place’ and opting for in-home care has never been stronger. Most Australians would understandably prefer to stay in their own home, surrounded by their family and memories, whilst remaining close to their local community, rather than moving into residential aged care.

Professional in-home support, whether it be nursing care, home modifications, or daily care, comes with a hefty price tag that is constantly rising. For many retirees, the challenge to care isn’t a lack of wealth; it’s that the wealth is locked inside their home – an asset itself which likely surged in value over recent years.

If you are over 55 and own your home, a reverse mortgage is a practical way to unlock that value and use your property equity to fund the care you or your loved one needs today, all while avoiding selling your family home.

Record Equity and Rising Care Costs

Australia is experiencing some of the highest inflation it has ever seen, pushing the Australian property market to record new heights in 2026, with median house prices nationwide well above $1 million. For long-term homeowners in cities such as Sydney, Brisbane, and Perth, this has created significant equity in their property.

At the same time, though, the cost to stay in your own home has changed. Whilst the government’s support at home program (which has recently been replaced with Home Care Packages) provides vital funding, there is often a significant gap between the subsidy and the actual cost that you may need to pay. The increased demand for home care services created by the subsidies has also driven up prices. On top of this, the cost of local services to future-proof care at home has increased, making the installation of a walk-in shower, stairlifts, and rails even more expensive.

How You Can Use a Reverse Mortgage for Home Care

A reverse mortgage allows you to access a portion of your home’s value as a tax-free lump sum or regular income stream. This differs from a regular home loan: there are no mandatory monthly repayments; interest accrues over time, and the loan is repaid only when you sell the home, typically when you move into permanent residential care or pass away.

Why Consider a Reverse Mortgage for In-Home Care?

With a reverse mortgage, you maintain full ownership and the right to live in your family home for as long as you choose. You also don’t have to access the money at once; most clients set aside a cash reserve and draw on the funds only as the need for care increases. Interest is applied only to the amount drawn, and the total loan is repaid when the property is sold.

It is a common misconception that reverse mortgages aren’t safe. That couldn’t be further from the truth! They are strictly regulated, and all reverse mortgages are protected by the No Negative Equity Guarantee, ensuring you or your estate never owes more than the value of the home.

Is a Reverse Mortgage the Right Way for Me to Access Care at Home?

Reverse mortgages are a long-term financial decision, and it’s our job to ensure our customers are fully informed and that a reverse mortgage is a suitable option for them before they enter into one. When considering the benefits, it is worth comparing the costs of residential care with those of staying in your own property and receiving care at home.

At Your Home Equity, we recommend discussing these options with your family, and it is a mandatory requirement for all borrowers to seek independent advice. As specialist brokers, we can help you compare the rates and features to find a structure that supports your specific care goals.

Take the Next Steps

Funding home care shouldn’t require you to sell your family home. If you want to see how your equity could help support your care, we’re here to help.

Download our free guide and get a breakdown of the reverse mortgage process. Alternatively, you can complete our free reverse mortgage calculator and discover your eligibility requirements. Or speak to us in person by booking a no-obligation free consultation with a licensed broker to discuss your options.

The information in this article is general in nature and has been prepared without taking into account the needs, objectives, or financial situation of any particular individual. Individuals should consider their own circumstances and, if necessary, seek professional advice. All reverse mortgage products are subject to the terms, conditions and approval criteria of the lenders and fees and charges apply.

Equity Mortgage Specialists Pty Ltd trading as Your Home Equity / Corporate Credit Representative (No. 530659) and Scott Phillips, Authorised Credit Representative (No. 547787) of QED Services Pty Ltd trading as Pursuit Broker Services / Australian Credit Licence 387856 / ACN 147 272 295